Mortgage Forbearance Explained

Mortgage Forbearance Explained helps homeowners understand temporary payment relief, what a forbearance agreement may do, what it usually does not do, and what questions should be asked before accepting a forbearance plan.

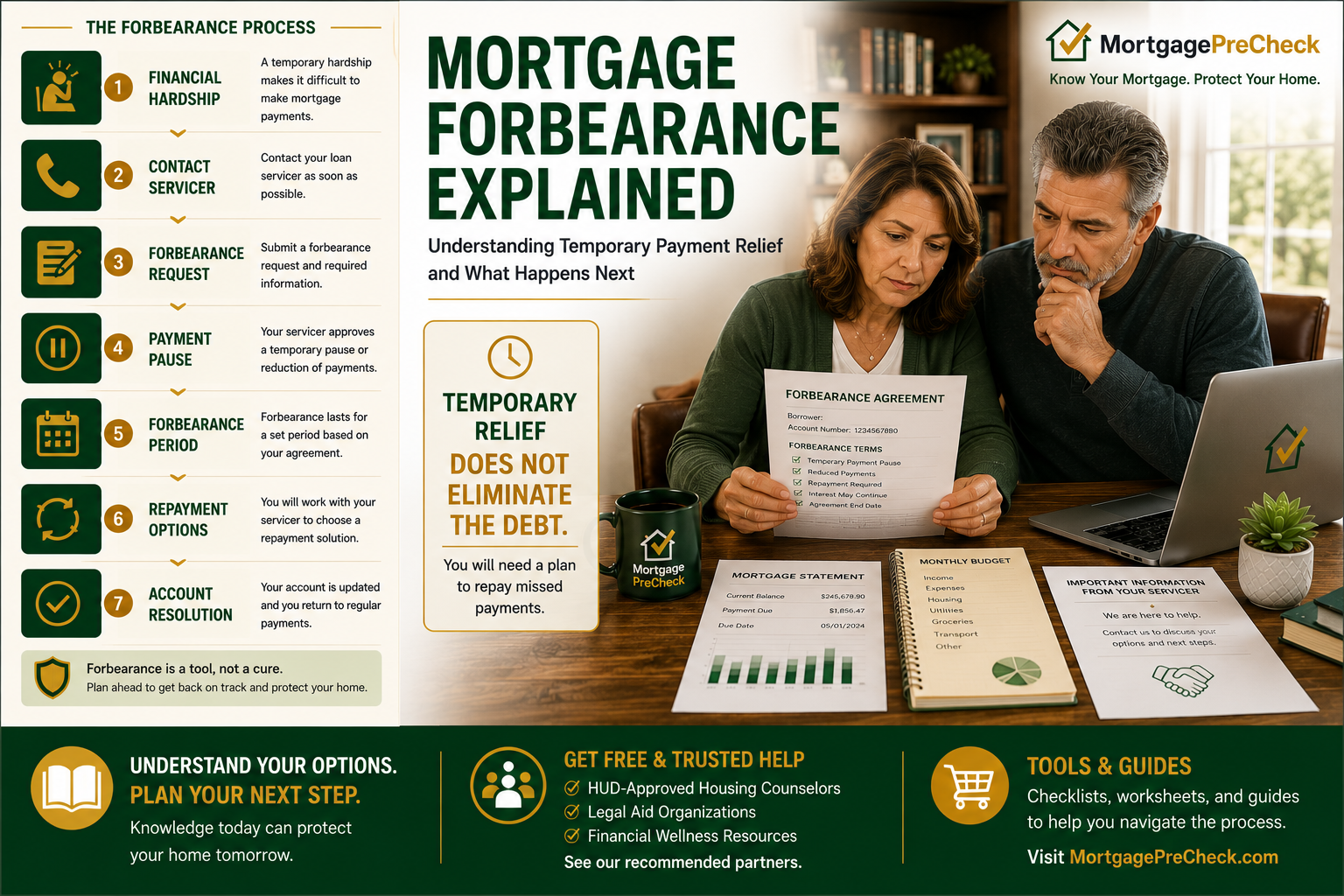

Mortgage forbearance is commonly discussed when a homeowner experiences a temporary hardship and cannot make regular mortgage payments for a limited period. The servicer may agree to pause or reduce payments temporarily, depending on the loan type, investor rules, program requirements, and account status.

MortgagePreCheck Tip: Mortgage forbearance is generally a temporary payment arrangement. It usually does not eliminate the amounts owed. Homeowners should ask how missed payments will be handled after the forbearance period ends.

Important Framework: Hard-Money Lending Assumption

This article, like the prior MortgagePreCheck educational articles, is written from the conventional hard-money lending framework used in most mortgage servicing communications, consumer guidance, and industry documents.

Under that framework, the loan is treated as a transaction where a lender advanced money, the borrower received the benefit of those funds, and the borrower is expected to repay the mortgage debt according to the loan documents.

MortgagePreCheck uses this framework for public-facing educational content because most servicer notices, mortgage statements, escrow analyses, forbearance letters, loan modification offers, investor guides, and consumer-facing resources are written from that perspective.

Mortgage Forbearance Explained: The Basic Idea

Forbearance is a temporary arrangement that may allow a homeowner to pause or reduce mortgage payments for a limited time.

The purpose is usually to give the homeowner time to recover from a short-term hardship and avoid immediate escalation of delinquency.

Forbearance is not usually a permanent solution. It is a temporary bridge that must eventually be followed by a repayment, deferral, modification, reinstatement, or other resolution plan.

When Forbearance May Apply

Mortgage forbearance may be considered when a homeowner has a temporary hardship that affects the ability to make regular payments.

Common hardship events may include:

- Temporary job loss

- Reduced income

- Medical hardship

- Natural disaster

- Unexpected household expense

- Temporary business disruption

- Death or illness in the household

- Other short-term financial hardship

What Forbearance Usually Does

A forbearance plan may temporarily pause or reduce the required monthly mortgage payment.

The plan may identify the start date, end date, payment amount during the forbearance period, reporting terms, and what happens when the forbearance ends.

The homeowner should carefully review the written forbearance agreement before relying on any verbal explanation.

What Forbearance Usually Does Not Do

Forbearance does not usually erase the missed payments.

It does not automatically reduce the principal balance, eliminate interest, cancel escrow obligations, or permanently change the loan terms unless the written agreement or later resolution option says so.

Homeowners should not assume that paused payments disappear. The unpaid amounts usually need to be addressed later.

What Happens After Forbearance?

The end of forbearance is often the most important part of the process.

When the forbearance period ends, the servicer may review the account for available exit options. These may include repayment, deferral, reinstatement, loan modification, or another loss mitigation option depending on program rules and eligibility.

Homeowners should ask about exit options before the forbearance period ends, not after the account becomes more difficult to resolve.

Common Forbearance Exit Options

Forbearance exit options may vary by loan type and investor rules.

- Full reinstatement

- Repayment plan

- Payment deferral

- Loan modification

- Extension of forbearance, if available

- Other loss mitigation review

Full Reinstatement

Full reinstatement means the homeowner pays all missed amounts at once to bring the account current.

This may not be realistic for many homeowners unless the hardship was short and funds are available.

Before choosing reinstatement, homeowners should ask for a written reinstatement amount and confirm the deadline for payment.

Repayment Plan

A repayment plan may allow the homeowner to catch up missed payments over time.

The homeowner may be required to make the regular monthly payment plus an additional amount until the missed payments are repaid.

This option may work when the homeowner can afford more than the regular monthly payment after the hardship ends.

Payment Deferral

A payment deferral may move missed payments to a later point in the loan timeline, depending on program rules.

Deferred amounts may become due at payoff, refinance, sale, maturity, or another specified event.

Homeowners should ask whether deferred amounts accrue interest and when the deferred amount must be paid.

Loan Modification After Forbearance

If the homeowner cannot afford reinstatement or repayment, the servicer may review the account for a loan modification.

A modification may change certain loan terms and create a new payment structure. The terms depend on the program and review results.

Homeowners should compare the modified payment, interest rate, term, escrow amount, deferred balance, and capitalized arrears before signing any modification documents.

Credit Reporting Considerations

Homeowners should ask the servicer how the forbearance will be reported to credit bureaus and whether the reporting depends on the account status before the forbearance began.

Credit reporting rules and program requirements may vary depending on the loan type, timing, hardship program, and applicable law.

Any credit reporting concern should be addressed in writing with the servicer.

Documents to Review First

Before accepting or exiting forbearance, homeowners should gather the documents needed to understand the arrangement.

- Current mortgage statement

- Payment history

- Forbearance agreement

- Servicer hardship letter or approval notice

- Escrow analysis, if applicable

- Loss mitigation application, if required

- Budget worksheet

- Repayment or deferral proposal

- Loan modification offer, if applicable

- All servicer correspondence

Questions to Ask Before Accepting Forbearance

- How long will the forbearance last?

- Are payments paused or reduced?

- Will late fees be charged during the forbearance period?

- How will the account be reported to credit bureaus?

- Will escrow payments continue during forbearance?

- What happens when the forbearance period ends?

- Will missed payments be due all at once?

- Will repayment, deferral, or modification be available?

- Can the servicer provide the terms in writing?

- What deadlines apply?

MortgagePreCheck Tip: The most important question is not only whether forbearance is available. The most important question is what happens after forbearance ends.

When Forbearance May Require Closer Review

Forbearance may require closer review when the homeowner does not understand the exit terms, when the servicer gives conflicting explanations, when a lump-sum repayment is demanded unexpectedly, or when the written agreement does not match the verbal explanation.

Closer review may also be appropriate if the account was already delinquent before forbearance, if the loan was transferred during the forbearance period, if credit reporting appears inaccurate, or if foreclosure activity is pending.

Related Mortgage Education Center Articles

Additional Educational Resources

Additional consumer mortgage information is available through the Consumer Financial Protection Bureau Mortgage Resources and general legal reference materials are available through Cornell Law School’s Legal Information Institute.

MortgagePreCheck Summary

Mortgage forbearance is temporary payment relief that may pause or reduce payments for a limited period during a hardship.

Forbearance usually does not eliminate the debt. The missed amounts must typically be addressed through reinstatement, repayment, deferral, modification, or another resolution option.

Understanding mortgage forbearance helps homeowners ask better questions before entering a plan and prepare for what happens when the forbearance period ends.

|

Previous Article

Loan Modification Explained |

MORTGAGE

EDUCATION CENTER |

Next Article

Understanding Default Notices |