Loan Modification Explained

Loan Modification Explained helps homeowners understand how a mortgage loan modification may change payment terms, what documents may be required, and how the review process commonly works.

A loan modification is one possible loss mitigation option. It may be offered when a homeowner has experienced a hardship and the servicer determines that changing certain loan terms may help create a more manageable payment structure.

MortgagePreCheck Tip: A loan modification is not the same as a refinance. A refinance usually replaces the loan with a new loan. A modification changes terms of the existing mortgage account.

Loan Modification Explained: The Basic Idea

A loan modification changes one or more terms of an existing mortgage loan. The purpose is usually to help resolve delinquency, reduce payment pressure, or create a sustainable payment arrangement.

The specific terms of a modification depend on the loan type, investor rules, servicer guidelines, hardship, account status, and available programs.

Not every homeowner qualifies for a loan modification, and not every modification lowers the payment. Homeowners should carefully review any offer before accepting it.

How a Loan Modification May Change the Mortgage

A loan modification may change different parts of the loan depending on the program and review results.

Common modification changes may include:

- Changing the interest rate

- Extending the loan term

- Adding missed payments to the balance

- Creating a new monthly payment

- Deferring part of the balance in some cases

- Changing the repayment structure

- Resolving past-due amounts through new terms

Why Homeowners Request Loan Modifications

Homeowners may request a modification when they cannot afford the current mortgage payment, have fallen behind, or need a long-term solution after a hardship.

Common hardship situations may include job loss, reduced income, medical expenses, divorce, household income changes, unexpected expenses, or increased mortgage-related costs.

The servicer usually reviews the homeowner’s financial information to determine whether a modification option is available.

Loan Modification vs. Forbearance

Forbearance is usually temporary. It may pause or reduce payments for a limited period, but the unpaid amounts still need to be addressed later.

A loan modification is usually intended to create a more permanent payment structure by changing terms of the loan.

Some homeowners may move from forbearance into a deferral, repayment plan, or loan modification depending on the program and eligibility.

Loan Modification vs. Repayment Plan

A repayment plan usually helps a homeowner catch up missed payments by paying the regular payment plus an additional amount for a period of time.

A loan modification may be reviewed when a repayment plan is not affordable or when a longer-term adjustment is needed.

The right option depends on the homeowner’s financial situation and the loan program.

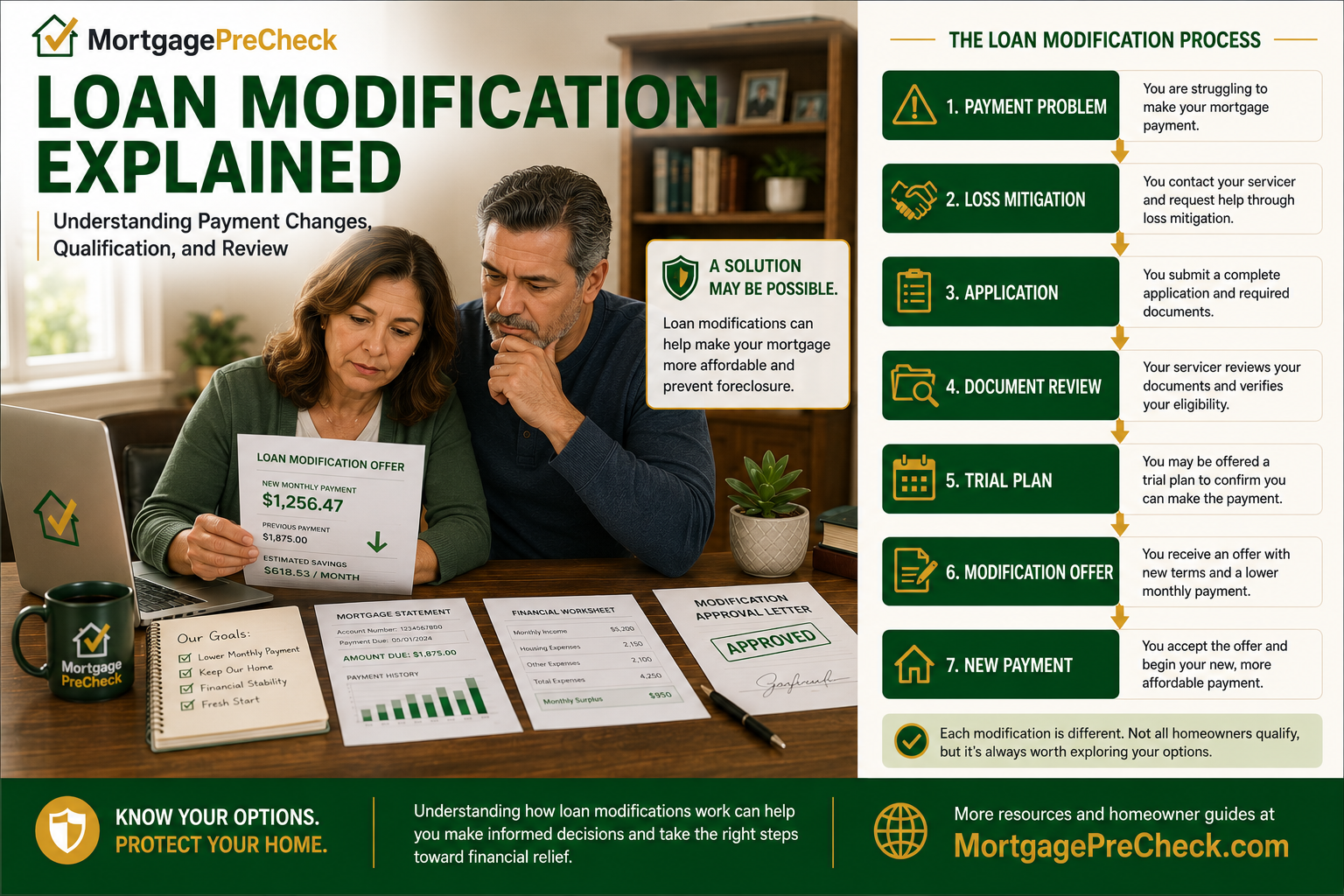

The Loan Modification Review Process

The loan modification process often begins with a loss mitigation application.

Step 1: The homeowner contacts the mortgage servicer and asks about available assistance options.

Step 2: The servicer provides application instructions and document requirements.

Step 3: The homeowner submits a complete application and supporting documents.

Step 4: The servicer reviews the documents for completeness.

Step 5: The servicer evaluates the homeowner under available program rules.

Step 6: The homeowner may receive a trial plan, denial, request for additional documents, or modification offer.

Step 7: If offered, the homeowner reviews the new terms before deciding whether to accept.

Trial Payment Plan

Some modification programs require a trial payment plan before a permanent modification is offered.

A trial plan usually requires the homeowner to make several scheduled payments to show that the proposed modified payment may be affordable.

Homeowners should carefully review the trial plan terms, payment due dates, and what happens after the trial plan is completed.

Modification Offer

If a homeowner is approved for a modification, the servicer may provide written documents showing the new terms.

The offer may identify the new payment amount, interest rate, loan term, capitalized arrears, deferred balance, escrow amount, and effective date.

Homeowners should review the documents carefully and ask questions before signing.

Documents to Review First

Before accepting a loan modification, homeowners should compare the proposed terms with the existing loan records.

- Current mortgage statement

- Prior mortgage statement

- Payment history

- Loss mitigation application

- Trial payment plan, if applicable

- Modification offer

- Mortgage Note

- Escrow analysis

- Hardship documents

- Servicer correspondence

Questions to Ask Before Accepting a Modification

- What will the new monthly payment be?

- Will the interest rate change?

- Will the loan term be extended?

- Will missed payments be added to the balance?

- Will any amount be deferred?

- Does the new payment include escrow?

- Will the escrow payment change later?

- What happens if a trial payment is missed?

- Is the modification temporary or permanent?

- Can the servicer provide the final terms in writing?

MortgagePreCheck Tip: Before signing a modification, compare the old payment, new payment, principal balance, interest rate, term, escrow amount, and any deferred or capitalized amounts.

When a Loan Modification May Require Closer Review

A loan modification may require closer review when the new payment is not affordable, when the balance increases unexpectedly, when escrow is not clearly explained, or when the written offer does not match what the homeowner was told.

Closer review may also be appropriate if the homeowner believes documents were submitted but not reviewed, if a denial is unclear, if a trial plan was completed but no final modification was issued, or if foreclosure activity is pending.

Related Mortgage Education Center Articles

Additional Educational Resources

Additional consumer mortgage information is available through the Consumer Financial Protection Bureau Mortgage Resources and general legal reference materials are available through Cornell Law School’s Legal Information Institute.

MortgagePreCheck Summary

A loan modification may change terms of an existing mortgage loan to help address delinquency or payment hardship.

The review process usually involves a loss mitigation application, financial documents, servicer review, and a written decision or offer.

Understanding how loan modifications work helps homeowners ask better questions, compare proposed terms, and make more informed decisions before accepting a new payment structure.

|

Previous Article

What Is Loss Mitigation? |

MORTGAGE

EDUCATION CENTER |

Next Article

Mortgage Forbearance Explained |