Mortgage Servicing Explained

Mortgage Servicing Explained helps homeowners understand who collects mortgage payments, who manages escrow, why mortgage companies may change, and what role a mortgage servicer plays after closing.

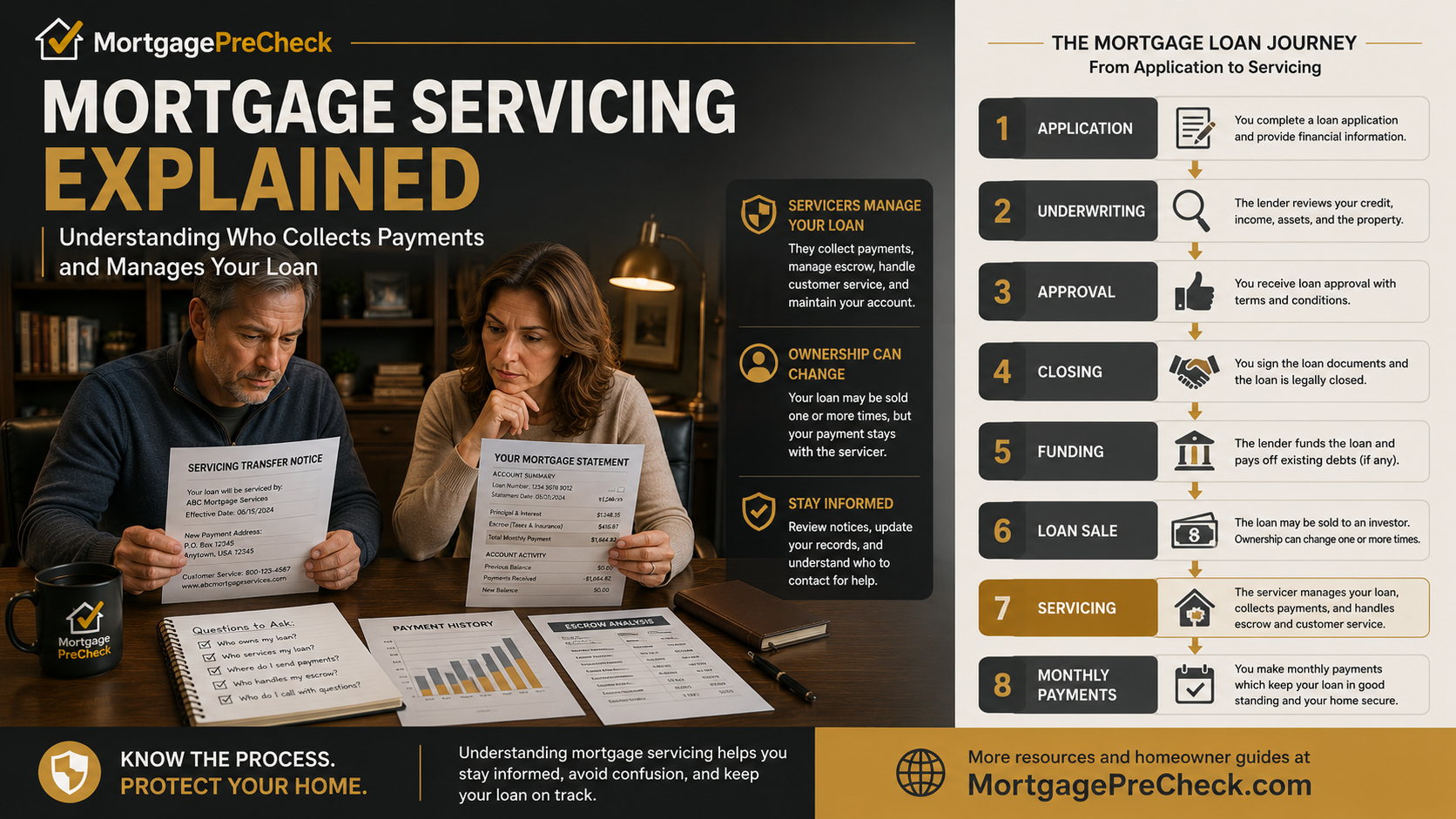

Many homeowners believe the company collecting the monthly payment is always the lender or owner of the loan. In many cases, that is not correct. The mortgage servicer may be different from the original lender, different from the investor, and different from the company that owns the loan.

MortgagePreCheck Tip: A mortgage servicer usually manages the account. The servicer may collect payments, send statements, manage escrow, process notices, and communicate with the homeowner, even if another party owns the loan.

Mortgage Servicing Explained: The Basic Idea

Mortgage servicing is the ongoing administration of a mortgage loan after closing. Once the loan is active, someone must collect payments, apply funds, send statements, maintain records, manage escrow, and respond to homeowner inquiries.

The company responsible for these tasks is commonly called the mortgage servicer.

The servicer’s role is administrative, but it can have a major impact on the homeowner’s monthly experience because the servicer is usually the company the homeowner hears from most often.

What Does a Mortgage Servicer Do?

A mortgage servicer may perform many tasks connected to the loan account.

- Collecting monthly mortgage payments

- Sending mortgage statements

- Applying payments to principal, interest, escrow, fees, or suspense

- Managing escrow accounts

- Paying property taxes from escrow

- Paying homeowners insurance from escrow

- Sending annual escrow analyses

- Handling customer service requests

- Processing payoff requests

- Managing loss mitigation or modification communications

- Sending default or account notices when required

Servicer vs. Lender vs. Investor

The lender is commonly the company that originated or funded the mortgage loan at closing.

The investor or owner may be the party that owns the beneficial interest in the loan after it is sold, transferred, assigned, or securitized.

The mortgage servicer is the company that manages the account and collects payments from the homeowner.

In some cases, the same company may serve more than one role. In other cases, the lender, investor, trustee, master servicer, and subservicer may all be different parties.

Why Mortgage Servicers Change

Mortgage servicing can change during the life of a loan. A homeowner may receive a notice stating that one servicer is leaving and another servicer is taking over.

- Servicing rights were sold or transferred

- The loan was sold to a different investor

- The prior servicer stopped servicing the loan

- A subservicer was assigned

- A company merger or acquisition occurred

- The loan was moved to a different servicing platform

- The account required specialized servicing

What Is a Servicing Transfer?

A servicing transfer occurs when one company stops servicing the loan and another company begins servicing the loan.

The homeowner may receive a goodbye letter from the prior servicer and a welcome letter from the new servicer. These letters should identify the transfer date, the new servicer, customer service information, payment instructions, and where future payments should be sent.

A servicing transfer should not change the basic loan terms by itself. The Mortgage Note and related loan documents continue to control the repayment obligation.

What Homeowners Should Review After a Servicing Transfer

After a servicing transfer, homeowners should compare account information carefully.

Step 1: Keep the goodbye letter and welcome letter.

Step 2: Compare the last statement from the prior servicer with the first statement from the new servicer.

Step 3: Confirm the principal balance, escrow balance, payment amount, due date, and payment history.

Step 4: Keep proof of payments made during the transfer period.

Step 5: Contact the new servicer in writing if the account information does not match prior records.

Escrow and Mortgage Servicing

Mortgage servicing often includes escrow administration. If the loan has an escrow account, the servicer may collect monthly escrow payments and use those funds to pay property taxes and homeowners insurance.

Servicers also prepare escrow analyses. These analyses estimate future tax and insurance expenses and identify whether the escrow account has a surplus, shortage, or deficiency.

Escrow issues are among the most common reasons homeowners contact mortgage servicers.

Payment Application

Mortgage servicers are responsible for applying payments according to the loan terms and servicing rules.

A payment may be applied to principal, interest, escrow, fees, charges, suspense, or other account categories depending on the amount paid and the status of the account.

If a payment is not applied as expected, the homeowner should review the statement, payment history, and servicer explanation.

Suspense Accounts

A suspense account may be used when the servicer receives a payment that is not enough to satisfy the full amount due or cannot immediately be applied as a full regular payment.

If funds appear in suspense, homeowners should ask why the funds were placed there, what amount is being held, and what is required to apply the funds to the loan account.

Documents to Review First

When reviewing mortgage servicing activity, homeowners should gather documents that show the account history and servicing changes.

- Current mortgage statement

- Prior mortgage statement

- Goodbye letter from prior servicer

- Welcome letter from new servicer

- Notice of servicing transfer

- Annual escrow analysis

- Payment history

- Property tax bill

- Homeowners insurance declaration page

- Correspondence from the servicer

Questions to Ask the Mortgage Servicer

- Are you the current mortgage servicer?

- Who owns or invests in the loan?

- When did you begin servicing the loan?

- What was the principal balance at transfer?

- What was the escrow balance at transfer?

- Were all prior payments received and posted?

- Are any funds being held in suspense?

- Were any fees, charges, or corporate advances added?

- Can you provide a complete payment history?

- Can you explain any change in payment amount?

MortgagePreCheck Tip: When a servicing issue arises, ask for the records. The mortgage statement, escrow analysis, payment history, and transfer notices usually show where the issue began.

When Mortgage Servicing May Require Closer Review

Mortgage servicing may require closer review when payments are missing, escrow balances do not match prior records, fees appear without clear explanation, or the new servicer’s records conflict with the prior servicer’s records.

Closer review may also be appropriate during default, loss mitigation, loan modification, foreclosure communication, insurance disputes, tax payment disputes, or after a servicing transfer.

Related Mortgage Education Center Articles

Why Did My Mortgage Company Change?

Understanding Your Mortgage Statement

What Is Escrow and Why Did It Increase?

Additional Educational Resources

Additional consumer mortgage information is available through the Consumer Financial Protection Bureau Mortgage Resources and general legal reference materials are available through Cornell Law School’s Legal Information Institute.

MortgagePreCheck Summary

Mortgage servicing is the ongoing management of a mortgage loan after closing.

The mortgage servicer may collect payments, send statements, manage escrow, apply payments, process account notices, and communicate with homeowners.

Understanding mortgage servicing helps homeowners review account changes, payment issues, escrow adjustments, servicing transfers, and communications from mortgage companies more effectively.

|

Previous Article

Homeowners Insurance and Your Mortgage |

MORTGAGE

EDUCATION CENTER |

Next Article

What Happens If I Miss a Mortgage Payment? |

Understanding Who Collects Payments and Manages Your Loan