Understanding Your Mortgage Statement

Understanding Your Mortgage Statement is one of the most useful skills a homeowner can develop. Your monthly statement can reveal how your payment is being applied, whether escrow changed, whether fees were added, and whether the account balance matches your expectations.

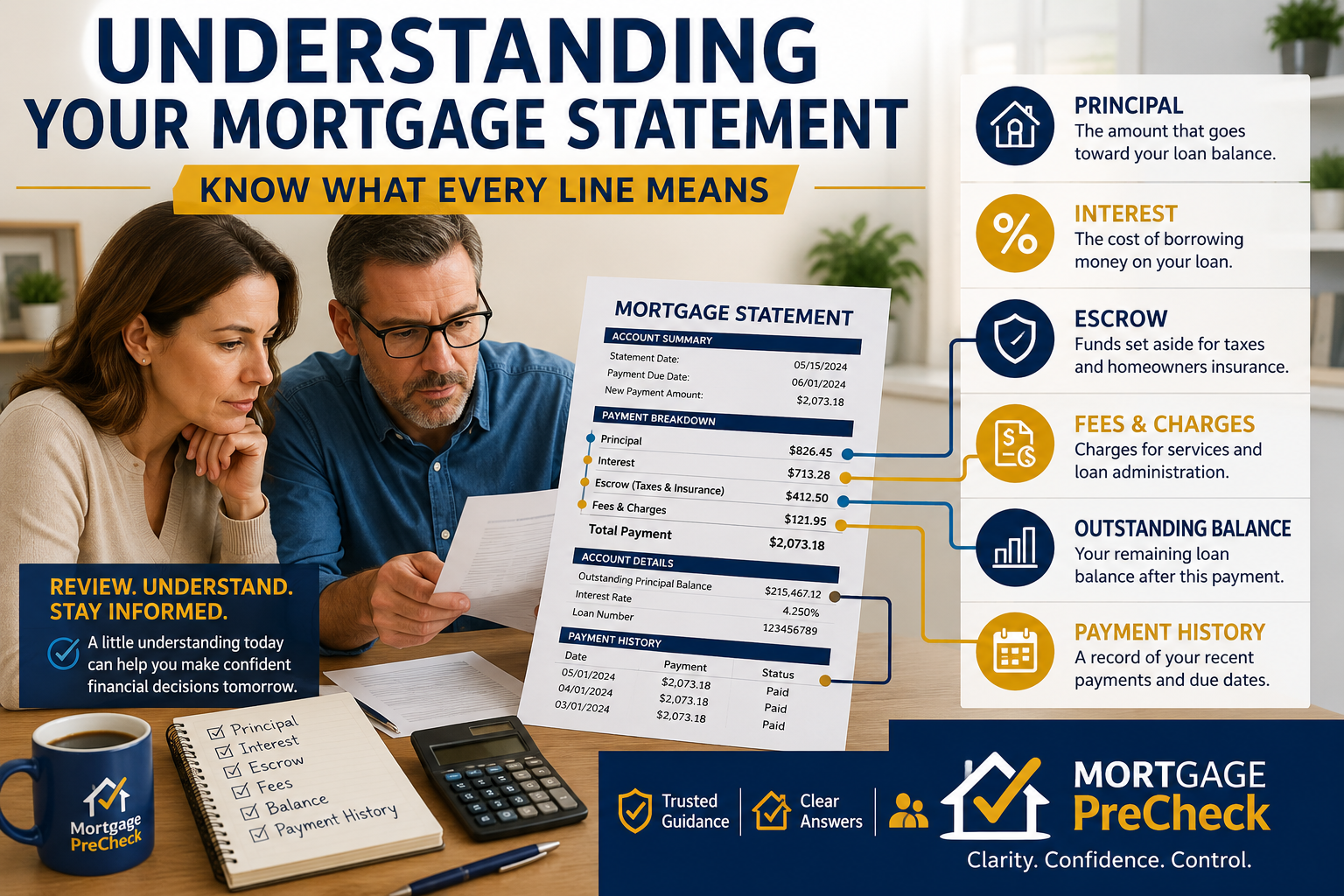

A mortgage statement is more than a payment reminder. It is a monthly snapshot of the loan account. When read carefully, it can help homeowners identify changes in principal, interest, escrow, fees, payment history, and servicing activity.

MortgagePreCheck Tip: Do not look only at the total payment due. Review each line item separately. The explanation for a payment change or account issue is often found in the details.

Understanding Your Mortgage Statement Basics

Most mortgage statements contain several sections. The exact layout may vary by servicer, but the same general information usually appears on most residential mortgage statements.

Common sections include:

- Payment due date

- Total amount due

- Principal and interest

- Escrow payment

- Fees and charges

- Outstanding principal balance

- Transaction activity

- Past payment information

- Servicer contact information

Principal

Principal is the unpaid loan balance. When a homeowner makes a regular mortgage payment, part of that payment may be applied to principal depending on the loan terms and payment schedule.

The principal balance should generally decrease over time when payments are made as scheduled. If the principal balance increases or does not decrease as expected, the homeowner should review the statement and payment history more closely.

Interest

Interest is the cost of borrowing money under the terms of the Mortgage Note. In the early years of many mortgage loans, a larger portion of the monthly payment may go toward interest than principal.

For fixed-rate loans, the interest rate generally stays the same unless the loan is modified or refinanced. For adjustable-rate loans, the interest rate may change according to the loan terms.

Escrow

Escrow is money collected by the mortgage servicer to pay property-related expenses such as property taxes and homeowners insurance.

If the escrow portion of the payment increases, the homeowner should review the escrow analysis, property tax bill, and insurance declaration page.

An escrow change can cause the total monthly mortgage payment to increase even when the principal and interest portion of the payment did not change.

Fees and Charges

Mortgage statements may show fees, late charges, inspection fees, recoverable expenses, corporate advances, or other account-level charges.

Homeowners should review any fee that appears on the statement and determine when it was added, why it was added, and whether the servicer has provided a clear explanation.

If a fee appears without explanation, the homeowner may wish to request a written account history or written clarification from the servicer.

Outstanding Principal Balance

The outstanding principal balance is the amount of unpaid principal remaining on the loan. This number is not always the same as the payoff amount.

A payoff amount may include interest through a specific payoff date, fees, escrow items, and other charges. Homeowners should not assume that the principal balance and payoff amount are identical.

Payment History

The payment history section may show recent payments, how payments were applied, and whether funds were applied to principal, interest, escrow, fees, or suspense.

Reviewing payment history is especially important after a servicing transfer, payment dispute, escrow change, or late-payment notice.

Suspense Account

A suspense account may appear when a servicer receives money that is not immediately applied as a full regular payment.

This can happen when a payment is short, when the servicer receives a partial payment, or when the amount received does not match the required amount due.

If a mortgage statement shows funds in suspense, the homeowner should ask how much is being held, why it was not applied, and what is needed to apply the funds to the account.

Past Due Amounts

If the statement shows a past due amount, the homeowner should compare the statement against payment records, bank records, and prior statements.

A past due amount may result from a missed payment, partial payment, payment posting issue, servicing transfer, fees, or suspense account activity.

Homeowners should keep copies of canceled checks, bank confirmations, online payment receipts, and any correspondence with the servicer.

Escrow Analysis and Statement Changes

A mortgage statement may change after an escrow analysis. If property taxes, homeowners insurance, or escrow projections increase, the escrow portion of the monthly payment may increase.

When a payment increases, homeowners should compare the new statement to the prior statement and identify which line item changed.

How to Review Your Mortgage Statement

Step 1: Confirm the payment due date and total amount due.

Step 2: Compare the current statement with the prior month’s statement.

Step 3: Identify changes in principal, interest, escrow, fees, or past due amounts.

Step 4: Review the payment history and confirm that recent payments were credited correctly.

Step 5: Check whether any funds were placed into suspense.

Step 6: Review the escrow section and compare it to the escrow analysis, tax bill, and insurance declaration page.

Step 7: Contact the servicer in writing if the statement does not match your records.

Documents to Compare

- Current mortgage statement

- Prior mortgage statement

- Payment receipts

- Bank confirmations

- Annual escrow analysis

- Property tax bill

- Homeowners insurance declaration page

- Servicing transfer notice

- Payment history from the servicer

Questions to Ask the Mortgage Servicer

- How was my most recent payment applied?

- Did any portion of my payment go to fees, suspense, or escrow shortage?

- Why did my total payment amount change?

- Were any late fees, inspection fees, or recoverable expenses added?

- What is the current escrow balance?

- Was an escrow analysis recently completed?

- Can the servicer provide a complete payment history?

- Does the statement reflect all payments made before and after any servicing transfer?

MortgagePreCheck Tip: A mortgage statement is a monthly account record. Saving each statement creates a paper trail that can be useful if a payment, escrow, servicing, or balance dispute later occurs.

When a Statement May Require Closer Review

A mortgage statement may require closer review when the payment amount changed without explanation, payments are missing, fees appear unexpectedly, escrow balances do not match prior records, or the statement conflicts with the homeowner’s own records.

Closer review may also be appropriate after a mortgage servicing transfer, loan modification, loss mitigation application, default notice, escrow shortage, or insurance premium increase.

Related Mortgage Education Center Articles

Why Did My Mortgage Payment Go Up?

What Is Escrow and Why Did It Increase?

Additional Educational Resources

Additional consumer mortgage information is available through the Consumer Financial Protection Bureau Mortgage Resources and general legal reference materials are available through Cornell Law School’s Legal Information Institute.

MortgagePreCheck Summary

Understanding your mortgage statement helps you identify how your payment is applied and whether changes occurred in principal, interest, escrow, fees, or account activity.

The best approach is to compare statements month to month, review each line item separately, and keep supporting documents in one file.

A homeowner who understands the mortgage statement is better prepared to identify payment changes, escrow adjustments, servicing transfer issues, and account discrepancies before they become larger problems.

|

Previous Article

What Is Escrow and Why Did It Increase? |

MORTGAGE

EDUCATION CENTER |

Next Article

Property Taxes and Your Mortgage |