What Is Escrow and Why Did It Increase?

What Is Escrow is one of the most common questions homeowners ask when their mortgage payment changes even though their loan balance, interest rate, or basic loan terms appear to be the same.

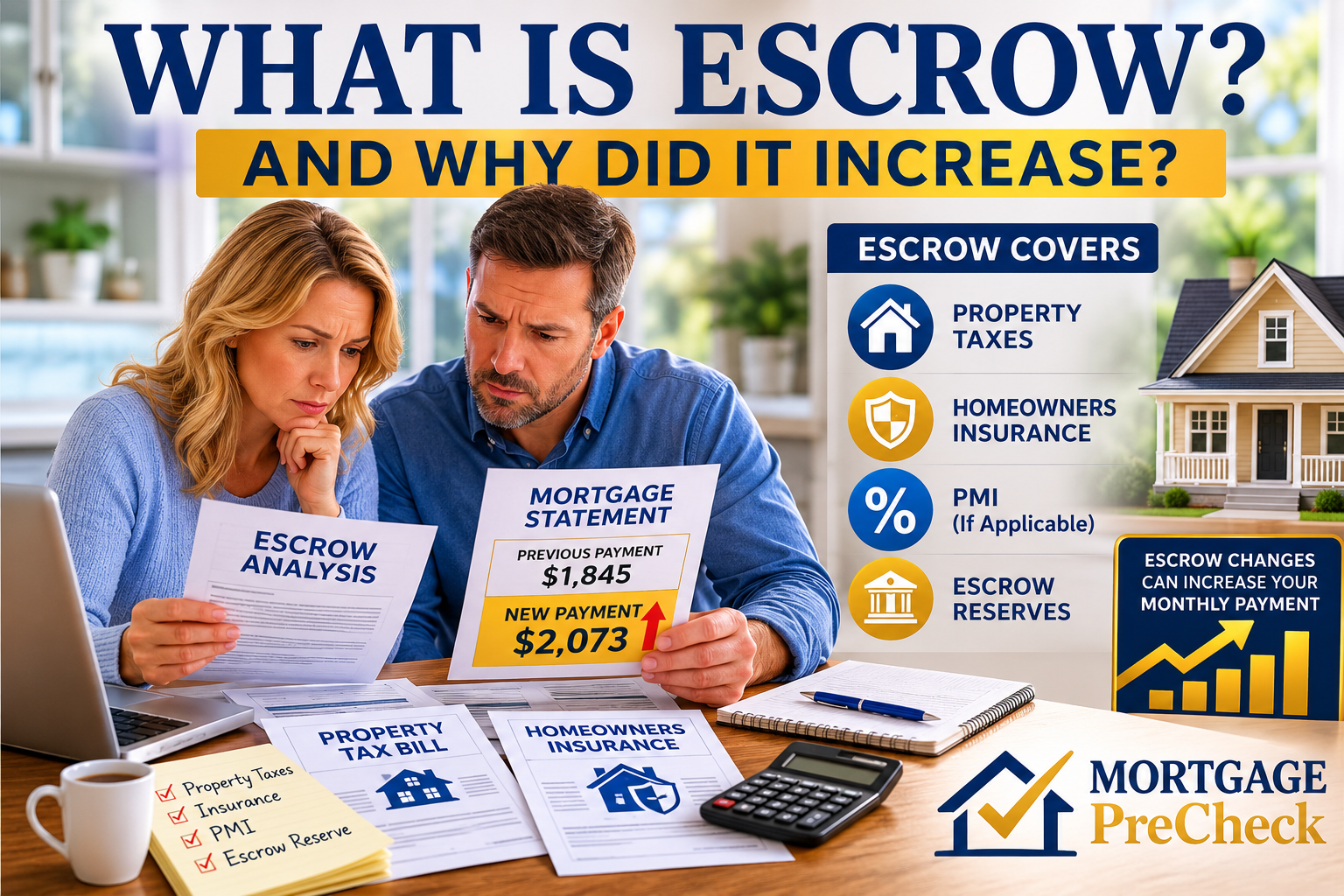

In a residential mortgage, escrow usually refers to money collected each month by the mortgage servicer to pay certain property-related expenses. These expenses commonly include property taxes and homeowners insurance. In some cases, escrow may also include mortgage insurance or other required items.

MortgagePreCheck Tip: An escrow increase does not always mean the lender changed the loan. Many escrow increases are caused by higher property taxes, higher insurance premiums, or a shortage from the prior escrow year.

What Is an Escrow Account?

An escrow account is a separate account maintained by the mortgage servicer to collect and pay certain expenses connected to the property.

Instead of the homeowner paying property taxes and homeowners insurance directly once or twice per year, the servicer may collect a portion of those estimated expenses each month as part of the total mortgage payment.

When the tax bill or insurance premium becomes due, the servicer uses money from the escrow account to make the payment.

Why Escrow Payments Can Increase

Escrow payments can increase when the amount needed to pay property taxes, homeowners insurance, or other escrowed items increases.

The most common reasons escrow payments increase include:

- Property taxes increased

- Homeowners insurance premiums increased

- The prior escrow account had a shortage

- The servicer changed projected future escrow expenses

- The property was reassessed

- The insurance carrier changed the annual premium

- The servicer corrected prior escrow calculations

Escrow Shortage

An escrow shortage occurs when the escrow account does not contain enough money to cover expected escrow payments.

For example, if the servicer estimated that property taxes would be lower than they actually were, the escrow account may not have enough money when the tax bill becomes due.

The servicer may pay the bill and then increase the homeowner’s monthly payment to recover the shortage and collect enough money for future escrow payments.

Property Tax Changes

Property taxes are one of the most common reasons escrow increases occur. Local tax authorities may increase assessments, tax rates, school levies, special assessments, or other property-related charges.

If the property tax bill increased, and the tax bill is paid through escrow, the mortgage servicer may increase the monthly escrow payment to account for the higher tax obligation.

Homeowners should compare the current tax bill with the prior year tax bill to determine whether property taxes caused the escrow increase.

Homeowners Insurance Changes

Homeowners insurance premiums may increase because of market conditions, replacement cost adjustments, claim history, policy changes, coverage changes, deductibles, or regional risk factors.

If homeowners insurance is paid through escrow, an insurance premium increase can cause the monthly mortgage payment to increase even if the principal and interest portion of the payment did not change.

Homeowners should review the insurance declaration page and compare the current annual premium to the prior annual premium.

Annual Escrow Analysis

Mortgage servicers generally review escrow accounts periodically. This review is often called an escrow analysis.

The escrow analysis estimates how much money will be needed to pay future property taxes, insurance premiums, and other escrowed expenses. It also identifies whether the escrow account has a surplus, shortage, or deficiency.

If the escrow analysis shows that future expenses are expected to increase, the monthly escrow payment may increase.

Escrow Surplus, Shortage, and Deficiency

A surplus means the escrow account has more money than the servicer expects to need under the escrow calculation.

A shortage means the escrow account balance is lower than required to maintain the projected escrow schedule.

A deficiency generally means the escrow account went negative because the servicer paid more from escrow than the account contained at the time of payment.

These terms may appear in the annual escrow analysis and can help explain why the monthly mortgage payment changed.

How to Review an Escrow Increase

When an escrow increase occurs, homeowners should separate the total monthly payment into its parts.

Step 1: Review the mortgage statement and identify the principal, interest, escrow, PMI, fees, and total payment amounts.

Step 2: Compare the new payment with the prior payment and determine which line item changed.

Step 3: Review the annual escrow analysis and identify any shortage, deficiency, or projected increase.

Step 4: Compare the current property tax bill with the prior year property tax bill.

Step 5: Compare the current homeowners insurance premium with the prior year premium.

Step 6: Contact the mortgage servicer in writing if the reason for the escrow increase is unclear.

Documents to Review First

- Current mortgage statement

- Prior mortgage statement

- Annual escrow analysis

- Property tax bill

- Homeowners insurance declaration page

- Insurance renewal notice

- Payment history

- Servicing transfer notice, if applicable

Questions to Ask the Mortgage Servicer

- What caused the escrow payment to increase?

- Was the increase caused by property taxes, insurance, shortage, or deficiency?

- What tax bill or insurance premium was used in the escrow calculation?

- Was there an escrow shortage from the prior year?

- Was there an escrow deficiency?

- Can the servicer provide the full escrow analysis?

- Can the servicer provide a payment history showing escrow deposits and disbursements?

- Did a servicing transfer affect the escrow calculation?

MortgagePreCheck Tip: The fastest way to understand an escrow increase is to compare the escrow analysis against the property tax bill and insurance declaration page. The cause is usually found in one of those documents.

When an Escrow Increase May Need Closer Review

An escrow increase may need closer review when the escrow analysis does not match the tax bill, when the insurance premium appears incorrect, when the servicer paid the wrong amount, or when the account shows unexplained shortage or deficiency amounts.

Closer review may also be appropriate after a servicing transfer if the prior servicer’s escrow balance does not match the new servicer’s records.

Related Mortgage Education Center Articles

Why Did My Mortgage Payment Go Up?

Why Did My Mortgage Company Change?

Additional Educational Resources

Additional consumer mortgage information is available through the Consumer Financial Protection Bureau Mortgage Resources and general legal reference materials are available through Cornell Law School’s Legal Information Institute.

MortgagePreCheck Summary

Escrow is money collected by the mortgage servicer to pay property-related expenses such as property taxes and homeowners insurance.

An escrow increase is usually caused by higher taxes, higher insurance premiums, a shortage, a deficiency, or a revised escrow projection.

Understanding escrow helps homeowners identify why a mortgage payment changed and what documents should be reviewed before accepting the new payment amount as accurate.

|

Previous Article

Why Did My Mortgage Company Change? |

MORTGAGE

EDUCATION CENTER |

Next Article

Understanding Your Mortgage Statement |