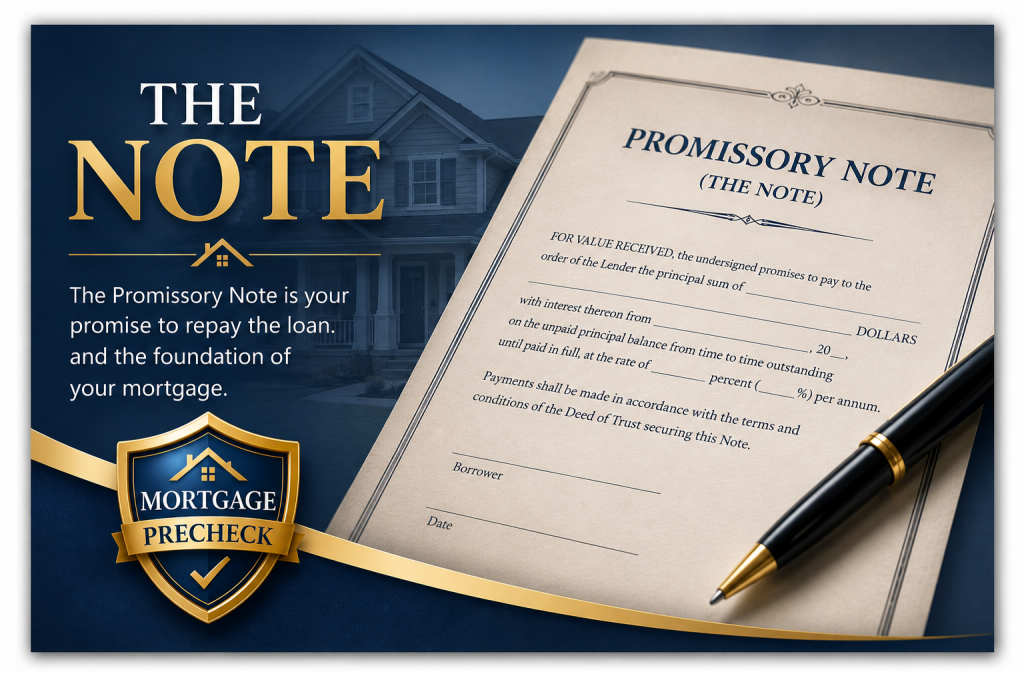

What is the Mortgage Note

The Mortgage NOTE also known as the Promissory Note, is, among all of the documents found in a typical mortgage package, is arguably the most important.

The mortgage NOTE is the document that contains the borrower’s promise to repay the loan according to agreed terms.

While many homebuyers focus on the interest rate, monthly payment, and amount due at closing, the mortgage NOTE establishes the repayment obligation and contains many of the terms that govern the loan relationship, which are rarely if ever explained to the Borrower prior to Closing.

Before signing any mortgage package, homeowners should take time to review and understand the NOTE.

The NOTE (aka Promissory Note) is a written promise to repay a specified amount under certain terms and conditions.

In a mortgage transaction, the NOTE typically identifies:

- The principal amount of the loan

- The interest rate

- The monthly payment amount

- The payment schedule

- The maturity date

- Late payment provisions

- Default provisions

- Acceleration provisions

The NOTE serves as the repayment committment by the borrower, notice I did not say “agreement” as there is only one party identified upon the NOTE, the Lender does not appear as a signatory and is not a party to that instrument except after you hadn it over to them at Closing…

There’s a lot more to this story which we will cover in the ensuing material.

The NOTE establishes the homeowner’s repayment obligation and outlines the terms under which repayment is expected.

For this reason, mortgage professionals consider the NOTE to be the most important documents within the mortgage package.

Homeowners should maintain a complete copy of the executed NOTE in their permanent records.

What to Do PRIOR TO Closing

Before signing, homeowners should carefully review the following asoects which appaer upon the mortgage NOTE, and even if you’ve done this before, today it is critical to ensure that you have three days to reveiw ALL of the documents before you go to closing.

Make sure you ask your mortgage company for copies of all documents because there are steps you need to take prior to Closing that you will not have time to perform or exceute after you get there.

Loan Amount

Confirm that the principal balance matches the amount expected from the transaction.

Interest Rate

Verify the stated interest rate and determine whether it is fixed or adjustable.

Monthly Payment

Review the required monthly payment and understand how it may change over time.

Payment Due Date

Confirm when payments begin and when they are due each month.

Late Charges

Mak sure you read EVERYTHING regarding any provisions reelated to late fees and delinquent payments; and what options you are entitled to in the event of an unexpected interruption of employment or salary. We will address this in more detail, just make not of this now for your matters.

Default Provisions

Understand what circumstances may trigger a default under the terms of the NOTE.

Acceleration Clause

Many NOTES contain an acceleration clause, these hidden problems that a typical homeowner i snot even aware of until something happens unexpectedly.

An acceleration clause generally permits the lender to demand immediate payment of the remaining balance if certain default conditions occur and/or to begin a foreclosure process within aa certain amount of time.

Homeowners should understand this provision in its entirety before signing. If you do ask questions before signing you are presumed to be in agreement with the terms and conditions which may or may not have even been explained or revealed to you prior to Closing.

Fixed-Rate vs. Adjustable-Rate Notes

Not all NOTES are identical. Some loans use fixed interest rates that remain constant throughout the loan term. Others use adjustable-rate structures that may change periodically according to the terms described within the NOTE. The latter is waht wa particallty reposnible for the banking disaster in 2008 when adjustable Note rates started to increase making it impossible for the homeowner to pay.

Understanding which type of NOTE is being signed is essential to understanding future payment obligations.

Questions Every Homeowner Should Ask

Before signing a NOTE, consider asking:

- Is the interest rate fixed or adjustable?

- How is the monthly payment calculated?

- Under what circumstances can payments change?

- What constitutes a default?

- What late fees may apply?

- What rights and responsibilities are described in the NOTE?

- Do I have a complete copy for my records?

*MortgagePreCheck Tip

The NOTE is more than a signature page. It is actually a security instrument you are issuing to the mortgage company and extending the option for them to sell it without your knowledge. It is one of the primary documents that establishes the repayment terms of the loan.

Before signing, homeowners should take time to read the NOTE carefully, ask questions about any provisions they do not understand, and retain a complete executed copy as part of their permanent mortgage records. your full understanding of what it is and how it works is critical to understanding the true source of the money being lent and who the actual creditor is in the transaction.

For mortgage education content, links to the following agencies are provided for your convenience and are the best authority sources. They are government or quasi-government educational resources recognized as highly authoritative.

Mortgage-specific resources:

CFPB Mortgage Resources

Official FHA homeownership and mortgage information.

Federal Housing Administration (FHA)

Homebuyer information:

FHA Homeownership Resources

Government housing and homeownership education.

HUD Homebuyer Resources

Housing counseling:

HUD Housing Counseling Program

Consumer protection and fraud prevention guidance.

Federal Trade Commission (FTC)

Consumer advice:

FTC Consumer Advice

Free homeowner education platform.

Fannie Mae HomeView®

Financial literacy and homeownership education.

Freddie Mac CreditSmart®

|

Previous Article

Secrets to Better Credit and Mrtgage Rates |

|

Next Article

What are the MORTGAGE and DEED OF TRUST Instruments |